🎮 back to the future

regulatory vulnerabilities in gaming

👋 Introducing: Alice Dawkins.

Alice and I have been in dialogue about the confusing, co-dependent, and obfuscated relationship between gaming and (big) tech.

We started considering the early millennium origins: for many of today’s elder millennials, gaming was the gateway to the early Internet. Children of the late nineties and early noughties explored the nascent digital sphere on CD-ROM desktop games, handheld consoles, and browser-based virtual worlds (e.g. Neopets).

Many of today’s tech regulation challenges have their antecedents from early gaming issues, like: content moderation, payments and alternative currencies, and identity verification. But gaming is almost always thought about and talked about completely separately from the tech sector: as a sister rather than a sub-component. Is that distinction still accurate? Who benefits from this classification and why might it have happened?

This raised questions for us, like:

How did gaming achieve this exceptional status?

What makes a gaming company a gaming company?

How does a gaming company differ from a digital platform?

Are today’s tech companies inevitably going to ‘pivot’ to gaming?

Is a metaverse just a persistent game?

Unlike the universalising force of most digital platforms, gaming companies have always been built with a specific end user in mind: gamers. The ‘platforms’ of the 2010’s swiftly became near-exclusive domains for key digitally distributed necessities: Facebook (social connections), Google Search (indexed information), Amazon (e-commerce). Online games and virtual worlds, in contrast, are true opt-in domains. Today’s networked platforms may anoint themselves as great creators and curators of community, but in many ways gaming companies mastered how to build community before anyone else.

Where gaming once imitated life, life (i.e. the Internet) now imitates gaming.

The regulatory history of [video] gaming is fascinating. Typically regulators have been concerned with content, gambling, and protecting minors. In the 90s, there was hysteria regarding violence in video games (first-person shooting games) which led to more age-based purchasing/playing restrictions.

Then, contemporary gaming became about volume and time. The key metrics for large gaming firms, such as: daily active users and session lengths, now mirror those of social media platforms - a preoccupation with the attention economy. As Protocol reports, gaming business models have three main phases: ‘pay-to-play’, in-built monetisation, and today’s NFT-powered ‘play-to-earn’ moment.

Gaming companies are courting public funding and incentives in similar ways to how ‘AI’-branded firms have seduced governments over the last decade for their purported job-creating potential and boon to national competitiveness. In a Canadian context, are Ubisoft or Electronic Arts the new ‘innovation’ darlings, on the verge of accumulating the hype and political capital enjoyed by incumbents like Google and Facebook, or the AI supercluster(s)?

As gaming companies scale and new entrants face meteoric rises, regulators and policy analysts must stay attentive to the narrative cycles likely to underline these journeys. It is crucial to remember how the immense success of ‘AI’ firms and digital platforms relied on seductive rhetorical diversions that boosted the potential of artificial intelligence and diluted its shortcomings, and query if gaming’s boosting of AR/VR follows a similar pattern.

While gaming seems to have has been carved out from “big tech” from a regulatory perspective, the spaces are no longer distinct:

Epic Games (Fortnite) is driving major competition investigations re: app store commissions and payment processing;

Google has Stadia cloud gaming service;

Apple is reportedly planning a game-subscription service akin to Netflix;

Google was reportedly planning to launch a “Netflix for Games” service;

Microsoft just bought Activision Blizzard.

Beyond the breathless web3 hypereel narratives, acquisitions and product announcements indicate the next technology giants are likely to evolve from and with today’s gaming companies. Big tech firms are obviously looking to gaming companies to inspire and drive their next phase of growth. What does a “pivot to gaming” mean for consumers and competition agencies?

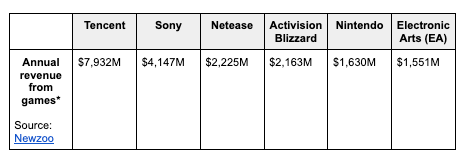

While technology firms of all kinds have “gamified” aspects of their offerings, this is a far more cohesive transformation. Games are big business, as revenue data from some of the best known companies shows.

As “big tech” merges/blurs with the gaming world, we are reminded once again that gaming has largely evaded the attention and scrutiny of regulators in fascinating ways.

This is most likely due to their status as a mode of ‘entertainment,’ that often sits together or with ‘gambling’ in regulation discussions.’ The gaming world also exemplifies self-regulation by the natural function of gameplay creating community-enforced norms and guardrails.

Gaming has also been at the forefront of: chat and messaging, payment, user experience, and the bundle of techniques sitting in the zones of augmented and virtual reality. The worlds built by gaming companies perform to far higher experiential standards than the ‘platforms’ assembled by social media operators. Consider how gaming companies hire some of the most skilled and specialised designers on the market: because offering intense, embodied, and immersive experiences is at the core of a game’s comparative advantage.

The line between consumer and worker can be a blurry one in gaming.

In some instances, gamers are also workers who create and maintain digital worlds. Contrast this to the typical “user” on a digital platform, who browses passively and has limited opportunities to positively maintain the experience for themselves or their peers. The answer to these uneven roles of user and gamer very likely lies in the differences in revenue model. The status of a gamer as a consumer is clear-cut and obvious: games, add-ons, and the devices they are played on are purchased in transactions. For social media, the profit model is famously convoluted. But both of these businesses have a shared desire to maximise engagement: the interesting detail lies in how this is achieved (recommender algorithms cf. vivid aesthetics) and how it is financed (advertising revenue cf. direct user sales).

Many predict that the next move from big tech is to mimic the best parts of gaming, to encourage their millions of assembled users into immersive and enveloping ‘social’ interactions. As the front pages of the internet become increasingly filled with clutter, distraction, and junk, the case for an aestheticised, ethereal online world feels compelling and comfortably escapist. If the big techs are entering the gaming business to recalibrate the user experience with arcade tactics, what comes next for consumers? Should consumers – and their protection agencies – be steeling themselves for new transactions, where search, email, chat, and e-commerce is paid for like a game?

🏛️ regs

Gaming companies seem to have escaped comprehensive attention of regulators because it gets lumped into entertainment. To date, gaming companies have only been regulated through an entertainment paradigm. Now, they are much more like big tech operators if not owned by them - big tech and gaming are codependent and intertwined.

As we look to the future to predict how big tech firms are pivoting and what current and future behemoths are doing, we need to look at gaming as a past gap but also a bit of a predictor for how companies are going to look and behave for users.

As government-led accountability agendas tighten for big tech, we should look to the various regulatory gaps that exist in gaming companies and watch for how big techs attempt to re-characterise themselves.

💰 riches

Governments occasionally court video game companies through tax incentives; growing these firms as they fall outside of a general tech accountability agenda.

Will experiential tech be the next innovation darling for place-based technology subsidies?

Vass Bednar is the Executive Director of McMaster University’s new Master of Public Policy in Digital Society Program and a Public Policy Forum Fellow.

|

|

Completely agree that games need more regulation. Free-to-play lends itself to massive user behaviour tracking akin to social media platforms. Also I recommend looking into Roblox: https://www.theguardian.com/games/2022/jan/09/the-trouble-with-roblox-the-video-game-empire-built-on-child-labour

More large game companies are pivoting towards what Roblox is doing.